Aave - Disrupting the Lending Industry

Level up your DeFi game and subscribe to the newsletter!

Hello DEFI WORLD Community,

Isa from Aave here, the protocol for money market creation on Ethereum where users can earn interest on deposits and borrow assets. The Aave Protocol was launched back in January, 2020, and already it has over $1.8 billion market size.

I’m super excited to tell you about how the Aave Protocol works, highlight some of the cool features, and give you an insight into what’s coming next!

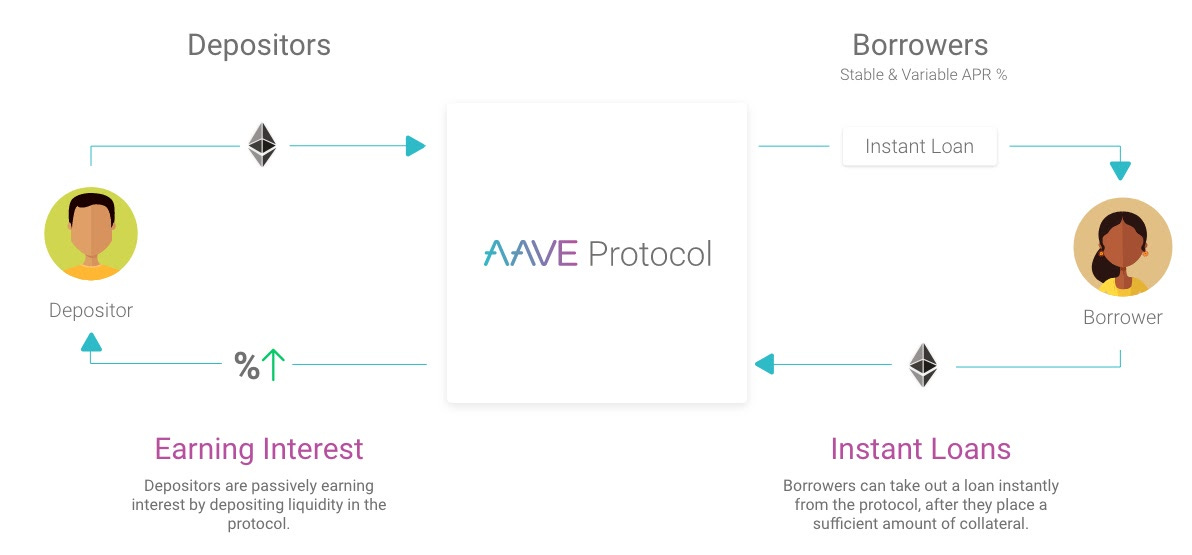

The Aave Protocol: An Overview

The Aave Protocol is an open source and non-custodial protocol for decentralised finance where users can deposit assets and earn interest on those assets while they’re loaned out to borrowers. Borrowers can borrow instantly, as long as they can put up enough collateral in another asset to support their loan. Borrowers can pay back their loan at any time, provided that they have enough collateral to support their position. The main Aave Market has 20 different crypto assets available to be deposited and borrowed.

Here you can find a helpful guide on how to get started with Aave!

Cool Features

The Aave Protocol has some cool features that make the experience better for both users and developers, including:

Flash Loans: These were the first uncollateralized loan option in DeFi. Flash Loans let developers borrow instantly without putting up any collateral, as long as they return the liquidity to the pool within one block transaction. If this doesn’t happen, the transactions are reversed to undo everything and ensure the safety of the funds in the pool. Learn more about Flash Loans and their use cases here.

Rate Switching: The Aave Protocol lets borrowers switch between variable and stable interest rates at any time, to ensure that you always get the best rates. Stable rates act as fixed rates in the short term, but they can be rebalanced to reflect changes in market conditions in the longer term. Stable rates are a great option for borrowers who want to have predictability, whereas variable rates are much more volatile.

Multiple Markets: The Aave Protocol currently has 2 markets: the Aave Market (the main one described above) and the Uniswap Market. The Uniswap Market allows Uniswap Liquidity Providers (LPs) to deposit their Uniswap LP tokens and use them as collateral. More markets are coming, with different use-cases and parameters.

Credit Delegation: Besides Flash Loans, Credit Delegation is another way to get an uncollateralized loan. Basically, Party A can deposit in Aave and delegate their credit line to Party B who can borrow against it. The terms and conditions of this loan are all laid out in a legal agreement with OpenLaw. The first Credit Delegation happened recently-- you can read about it here.

What’s next?

The “Aavenomics” proposal for tokenomics and governance was recently released, and governance is currently on testnet. The LEND token will be the governance token of the protocol, and soon LEND holders will be able to vote on governance updates. There will be a proposal to migrate from the LEND token to the AAVE token, and if this is voted on by the community, the AAVE token will be the protocol’s governance token.

Stay tuned for Aave V2, which will bring new features like fixed rate lending, gas optimizations, and more!

Finally, after a year-long application process, Aave’s UK branch called Aave Limited has received an Electronic Money Authorization (Revolut and Coinbase have the same license) from the Financial Conduct Authority. This means Aave can issue electronic money accounts and facilitate payments and currency conversions. This means UK users will be able to access DeFi directly from electronic money accounts, bringing the DeFi and FinTech spaces closer together. Eventually, the goal is for the whole Aave ecosystem to be able to benefit from these services. You can read more about this development here!

Feel free to follow Aave on twitter for more updates (and spicy memes) or talk to us in our Discord!

All information presented above is for educational purposes only and should not be taken as investment advice.